Picture a financial plan that strikes a balance between discipline and flexibility, giving both new and experienced investors a way to grow their wealth. Systematic Investment Plans, or SIPs, have become a key part of modern investment strategies because they offer a structured but flexible way to build wealth over time. SIPs have been around for decades, and they have slowly changed over time.

SIPs are now becoming more popular as a strong alternative to traditional investments because of their unique and powerful benefits. SIPs have a lot of great benefits, such as rupee cost averaging, the potential for exponential growth through compounding, and the ease of making regular, manageable contributions.

SIPs are appealing to people who want to save money in a disciplined way and make sure their financial future is safe because they are tailored to fit different financial goals. SIPs also give investors access to professional fund management, which makes it easier to manage their own money. This article goes into great detail about What is SIP and its benefits, including their history, benefits, and how they stack up against lump-sum investments.

We will look at how they help with financial discipline, risk management through diversification, and the most important things to think about before making SIP investments. We will help you start, run, and improve SIPs so that you can make a lot of money over time.

Understanding Systematic Investment Plans (SIPs)

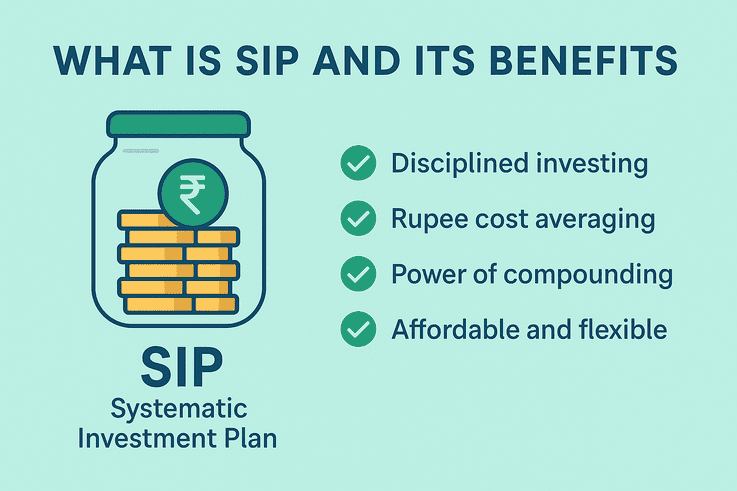

Systematic Investment Plans (SIPs) are a way to invest in mutual funds that is organised and disciplined. They are good for both new and experienced investors. SIPs are a good way to get into the habit of saving and investing regularly over time.

SIP nurture the habit of investing by making you invest a fixed amount of money at regular intervals, usually every month or every three months. This method cleverly deals with market volatility, which can lead to rash investment decisions based on changing market trends.

One of the best things about SIPs is that they use rupee cost averaging, which helps lessen the effects of market volatility. SIPs also let you make small, regular contributions, which makes them available to a lot of investors who want to slowly build wealth through the power of compounding.

What is SIP?

SIP stands for Systematic Investment Plan, which is a way to invest that makes it easy to make regular contributions to mutual funds.

With SIP method, investors can put a set amount of money into a chosen mutual fund scheme on a regular basis, like once a month or once a quarter.

You can start a SIP with as little as Rs. 500, and you can choose how much and how often to invest. This structure not only helps people stay on top of their finances, but it also encourages you to invest regularly.

SIPs let investors buy more fund units when prices are low and fewer units when prices are high. This is called “Rupee Cost Averaging.”

Over time, this can help investors by lowering the average cost per unit. In the end, SIPs use the power of compounding to help investors slowly grow their wealth.

The idea of Systematic Investment Plans (SIPs) has become very popular as a way to invest in mutual funds. SIPs were first introduced to help people develop a disciplined investment habit.

They let investors make regular, fixed contributions to a fund. The idea of rupee-cost averaging is what makes SIPs so appealing. It lets you buy more fund units when the market is down and fewer when it is up.

This not only spreads out the market risk, but it also keeps the cost of investments steady over time. SIPs became more flexible over time, letting investors change how much they invest based on their financial situation and goals. This change has made SIPs more appealing to a wider range of people, making them a flexible and popular way to invest, especially for people who want to build wealth and reach long-term financial goals.

Why Go with SIPs?

Systematic Investment Plans (SIPs) are a good way for people who want to build their wealth over time to invest. SIPs help people save money by letting them put fixed amounts of money into mutual funds on a regular basis.

This steady method makes it easier to avoid the problems that come with trying to time the market, which lowers the risk of losing money in the market. SIPs are easy and convenient because they take money out of a bank account automatically and make investing easier.

Also, SIP investments are usually cheaper, which makes them a good choice for investors who want to save money. Because SIPs require a smaller initial investment, more people can use them, which makes it easier to build wealth over time without putting too much strain on your finances.

Benefits of Rupee Cost Averaging:

Rupee Cost Averaging helps to even out investment costs by taking advantage of changes in the market. This strategy helps lower the cost per unit over time by buying more units of a mutual fund when the market goes down and fewer units when it goes up. The idea comes from Benjamin Graham’s book “The Intelligent Investor” and takes away the stress of timing the market, making the investment process more stable.

As investors invests on a regular basis, the total cost of their investments may go down. This encourages disciplined saving and good money management. Rupee Cost Averaging makes market conditions less scary by making sure that investments are made at regular intervals. This helps investors stay focused on their long-term financial goals.

The Power of Compounding in SIPs

With SIPs, compounding enables modest investments to eventually grow into substantial sums of money. Investors can profit from both principal and accrued returns by reinvesting returns.

The greatest benefit is obtained by starting early, which is consistent with risk tolerance and long-term financial objectives. Because SIPs are user-friendly and adaptable, investors can tailor their investments to suit their unique financial circumstances.

Additionally, they provide expert fund management, maximising returns through in-depth market research. These professionals are able to read market conditions and modify their plans to take advantage of fresh opportunities. SIPs from professionally managed mutual funds give investors the information and abilities they need to reach their financial objectives.

SIP vs Lump Sum Investment

SIPs and lump sum investments are two popular ways to invest in mutual funds. Each of these ways to invest has its own pros and cons, and they can all help you reach different financial goals and levels of risk.

With SIPs, you put a set amount of money into a mutual fund on a regular basis, usually once a month, for a long time. This method encourages people to save money in a disciplined way and helps them spread their investments across different market conditions.

A lump sum investment, on the other hand, means putting a lot of money into a mutual fund all at once. If the market is good, this could lead to big profits. But the lump sum strategy is riskier because you could enter the market at the wrong time. Investors can figure out which strategy works best for them by looking at these two options and seeing which one fits their financial situation, risk tolerance, and investment goals.

Key Differences

Mutual fund investment strategies include lump sum investments and Systematic Investment Plans (SIPs). SIPs encourage flexibility and discipline by requiring a fixed monthly contribution. They are appropriate for people who wish to gradually save money.

However, lump sum investments are bit riskier and require careful timing because they involve a significant amount of money. While lump sum investments strive for large returns because of increased market volatility, systematic investment plans (SIPs) offer a consistent, low-risk investment approach.

Each Approach Has Its Pros and Cons

Benefits of SIPs: Regular, automated investments promote the development of disciplined saving practices.

- By using rupee-cost averaging, it lowers market volatility.

- Allows for investment amount flexibility based on individual financial circumstances.

- Enables investments to be paused or stopped in response to life changes.

Drawbacks of lump sum investments include the potential for large returns in a favourable market.

- Has a greater chance of market collapse and demands a large initial investment.

- Demands a great deal of risk and market expertise.

- Depending on their risk tolerance and financial objectives, investors can select between lump sum and systematic investment plans (SIPs).

How SIPs Instill Financial Discipline with Regular Saving Habits

SIPs are a tactic for attaining financial objectives and encouraging financial discipline.

SIPs automate investments at predetermined intervals, encouraging saving and investing without market timing. They involve regular contributions to a mutual fund, encouraging consistent investment habits.

This approach helps avoid rash decisions influenced by market conditions and maintains a structured approach to personal finance management. SIPs encourage regular saving habits, which are crucial for accumulating long-term wealth.

The consistency of consistent contributions helps investors avoid the temptation to time the market or skip investments. This methodical approach aids investors in achieving their financial objectives and upholding consistent saving practices.

Long-term Wealth Creation

Through rupee-cost averaging, a methodical approach to investing that averages expenses over time, SIPs provide long-term wealth creation. This lessens stress and market swings. SIPs allow investors to start with smaller amounts and are structured and automatic, allowing them to stay disciplined and gradually build up wealth. Systematic investment plans are therefore a helpful tool for safeguarding financial futures.

Diversification Advantages of SIPs

By distributing investments across a variety of assets, Systematic Investment Plans (SIPs) are well-liked for portfolio diversification and market risk mitigation. By taking a methodical approach to financial objectives, they enable investors to gradually increase their wealth by holding a variety of stocks, bonds, and securities.

Mitigating Investment Risks

By distributing contributions over time and protecting against market swings, SIPs lower investment risks. To average out expenses and guarantee prudent risk management, they purchase units at various prices during various market phases using the rupee cost averaging principle. This enables investors to reach their financial objectives and adjust to shifting market conditions.

Portfolio Diversification

SIPs are important for a well-rounded portfolio because they let investors put money into different types of assets and keep their portfolios safe from market swings. They spread risks out over time, which lets investors take advantage of different market conditions and deal with different time frames and levels of risk.

Factors to Consider Before Starting an SIP

- Before you start, think about what your financial goals are.

- Figure out how much risk you’re willing to take and how long you want to wait.

- It’s important to have a disciplined and long-term investment plan.

- You can benefit from regular contributions and the benefits of rupee cost averaging.

Setting Investment Goals

Start a SIP to make sure your investment plan fits with your financial goals, like saving for retirement, buying a home, or paying for school. SIPs help people stay financially responsible by letting them make regular contributions, build wealth, and set goals without having to do market research.

Assessing Risk Appetite

When choosing the best SIP, it’s important to know how much risk you’re willing to take. This helps you split your portfolio into equity, debt, or hybrid funds, which is in line with your long-term financial goals. This assessment makes a balanced and varied investment plan that protects against bad asset performance.

Understanding Time Horizons

SIPs are great for long-term financial goals because they can handle short-term market changes and compound returns. By aligning their investment horizons with their financial goals, investors can make regular contributions, build wealth over time, and achieve significant growth by focussing on retirement or life events.

How to Start an SIP

- ✅ Know what you want to do with your money—Whether it’s retirement, a dream home, or your child’s education, clarity is the key

- 📊 Check your risk profile – Pick funds that fit your risk tolerance and time frame.

- 💡 Choose the right mutual fund scheme: We help you choose the best options for your needs.

- 📅 Choose how much and how often you want to SIP – With time and consistency, even a small amount each month can add up.

- 📝 Finish your KYC and paperwork – A simple, one-time process to get you ready to invest.

🚀 Are you ready to start your SIP journey? Contact us at www.vaaradhifinserv.com (Vaaradhi Finserv), and we’ll help you get started and guide you every step of the way!

Steps to Begin Investing in SIPs

Set clear financial goals and figure out how much risk you can handle before you start investing in SIPs. Think about debt funds or equity funds based on how stable or volatile they are. Use past performance to back up your choices. Figure out how much money you want to invest each month and SIPs will automatically buy units in mutual funds.

This makes sure that investments are made consistently and costs are spread out over time as net asset values (NAVs) keep changing. This will help you pick the right SIP plan for your needs.

Choosing the Right Mutual Fund Scheme

Choosing the right mutual fund scheme is very important for a successful SIP. Think about how much risk you’re willing to take and what you want to get out of your investments.

Look at how well funds have done in the past to see if it is reliable. Look at the expense ratio and exit loads to see what kind of returns you might get.

Know what assets are in each scheme’s portfolio and what risks they might face. Check how flexible the fund is in terms of pausing, stopping, or changing SIPs to make sure your investments fit your financial situation.

Setting Up and Managing SIP Investments

To set up a mutual fund SIP, you need to do KYC verification and make an auto-debit plan with your bank. Change the amount and frequency of your investments to fit your budget. Ask your fund provider if SIPs let you pause contributions when you have unexpected money problems. Use SIP calculators to keep track of your investment returns and make sure your assets grow in line with your financial goals.

Monitoring and Reviewing SIP Performance

For the best performance, it’s important to review SIPs on a regular basis. Rupee cost averaging helps keep the average cost per unit the same, which helps reduce market volatility. By following this structured plan, you can build your wealth over time by making steady investments. SIPs also let you compound, which means you can get bigger returns. They are flexible, so investors can change the amount and frequency to fit their financial goals.

Adjusting SIPs Based on Financial Goals

You can get much better investment results by customising SIPs to fit your financial goals, such as saving for retirement, paying for school, or buying a home. To be a good investor, you need to set clear financial goals.

SIPs are flexible, which means that investors can change their investments based on how much money they have. Regular contributions help you learn how to invest wisely, and SIP calculators help you plan your investments and make smart decisions based on your financial goals.